Fifty years ago, you could hardly rent a car, buy a tennis racket, crank up your stereo speakers, or stock up on cans of corned beef hash without putting money into the pockets of James Ling. As the head of Ling-Temco-Vought, the Dallas businessman ran more than 11 corporate subsidiaries that made consumer electronics, packaged meat, and even developed aircraft used in the Vietnam War.

Ling’s conglomerate came into being alongside others, like ITT Corp. and Litton Industries, in the booming years of the 1960s. The low interest rates and simplified stock valuation of the era allowed these giants to take unprecedented hold of diverse industries, and in 1968 this magazine pronounced “It Is Theoretically Possible for the Entire United States to Become One Vast Conglomerate Presided Over by Mr. James L. Ling.” Just two years later, Ling was forced out of LTV, and the capitalist juggernauts of the decade met with an unraveling of the house of cards they had built in quick acquisitions and sketchy stock exchanges.

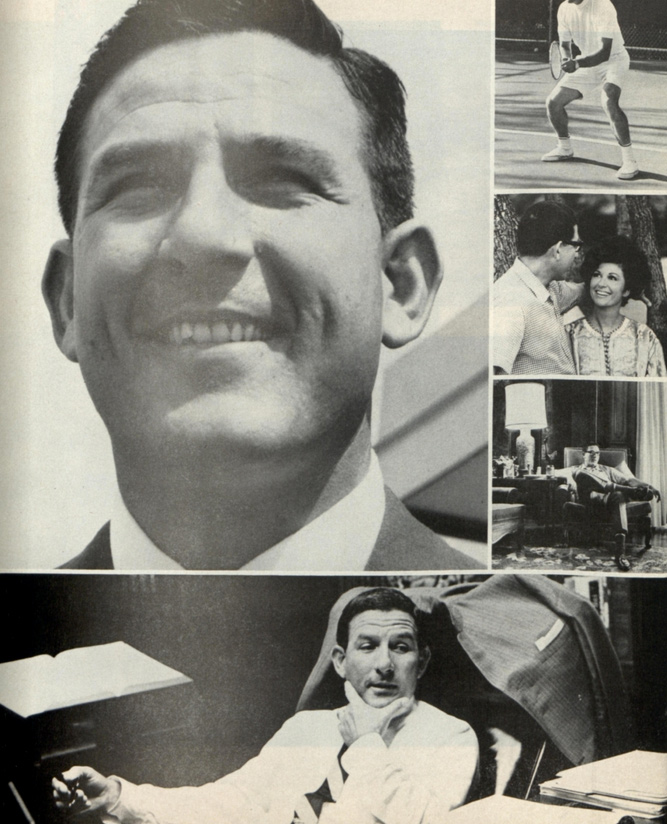

Ling was a postwar entrepreneur with a decidedly American life story. After his mother died from blood poisoning, Ling’s laborer father sent him to boarding school. He dropped out at age 14 and roamed the country doing odd jobs until he landed an opportunity as a journeyman electrician at an aircraft plant. Twenty-two-year-old Ling left for two years to serve in the Navy and furthered his skills as an electrician while maintaining equipment in the Philippines. Upon his return to Dallas, Ling was intent on transcending hourly wage work, so he sold his house and used the equity to start his own electrical contracting company.

The boldness and tendency for risk that characterized the ex-sailor’s foray into business would remain constant throughout Ling’s expansion. He hustled products and shuffled around finances to make it work for his small firm, garnering an industrial contract that he could barely fulfill. Within a few years, he was looking to go public in spite of an incredulous audience of Dallas business watchers. He hawked his stocks door-to-door and at a booth at the Texas State Fair and scrounged the money together with the help of some faithful investors.

By 1960, Ling-Temco was the 14th-largest industrial company in the country. Ling’s acquisitions over the coming decade dazzled investors as it appeared that he could make a company more profitable and efficient by swallowing it up. His business philosophy was based on the idea of synergy — or, in the ’60s, synergism — the concept that a conglomerate, as a whole, could be worth more than the sum of its parts. “What the sparsely educated Oklahoma poor boy discovered was that two plus two, properly added and managed with flair, can add up to seven or eight if you have enough brains and guts to handle the equation,” Don Schanche wrote of Ling in the Post.

While many American corporations formerly had taken part in vertical integration or horizontal integration (which stirred concern for monopoly), conglomeration in the postwar era — particularly in the ’60s — focused on diversification. Cornell University business historian Louis Hyman says, “It’s the first time that management is valorized as completely independent of the thing being managed. That’s how they justified these kinds of unrelated purchases.” The popularization of the MBA and the veneration of managerial science mystified the clever finances being wrought by conglomerate heads like Ling, who used debt and inflated stock valuation to grow their empires.

LTV’s stock price rose when they took on more subsidiaries, including Okonite, Wilson and Co., and Greatamerica Corp. Ling worked out complicated deals, then split the companies into smaller units, quickly selling the shares for more than the original value of the parent company. He discovered that revenue growth, even without profit growth, could make Ling and his shareholders a lot of money just by reorganizing balance sheets and continuing to acquire.

In Hyman’s recent book, Temp: How American Work, American Business, and the American Dream Became Temporary, he writes, “The real danger of conglomerates was not their power, but how their weakness perverted American corporations and helped to end the postwar prosperity.” Hyman believes the story of Ling’s — and nearly every other major American corporation’s — conglomeration years should be more widely known. Although the overall financial fallout was less acute than in 1929 or 2008, he says the lasting effects of conglomerates on the U.S. economy have been severe.

“My suspicion is that it led to the stagnation of the economy in the ’70s as people focused less on long-term investment and more on the fear of being conglomerated,” Hyman says. “It injected a measure of fear into American corporations.”

Ling’s business practices, under the guise of reflecting management genius, boiled down to a shell game in which longstanding, successful corporations were reorganized to the detriment of innovation and possible value creation. And he wasn’t alone: by the late ’60s, most of the 150 monthly mergers taking place were by conglomerates, which took up more than 90 percent of the Fortune 500. “Most American corporations that survived the 1960s figured out a way to handle conglomeration and deconglomeration,” Hyman says.

The force with which LTV grew led investors to believe it could never fail, and the Federal Trade Commission became concerned.

“The FTC already is worried enough about the growing conglomerate companies in the U.S. to have embarked on a long-term investigation,” Schanche wrote in the Post in 1968. “Ling has branded the probe ‘business McCarthyism’ and a witch hunt.”

The Justice Department filed an antitrust lawsuit against Ling after he acquired Jones and Laughlin Steel in 1968. Investors were troubled, especially since the suit coincided with other losses and a market downturn. The Times wrote, “LTV’s stock, which had traded for as much as $169 a share in 1967, plunged to a low of $4.25 the week Mr. Ling was ousted.” Ling was kicked out in 1970, and the once-gargantuan conglomerate, faced with low market prices, was forced into several divestures in the coming years.

Although the Justice Department’s investigations were timely, the reasoning for LTV’s downfall was in the market. Since Ling’s conglomerate was built on the premise that LTV’s high stock could be traded for the lower stock of his acquisitions, the Dallas man was in trouble (and in debt) when this scheme didn’t deliver.

LTV held on, through several bankruptcies, until 2000, but Ling found it impossible to continue his old ways in a new economy. He went into gas, oil, and real estate, bankrupting some companies and netting profit with others. His glory days were over, for good, and he had to part ways with his $3.2 million Dallas mansion.

In the shadow of the conglomeration years, economists rethought the merits of good management. Harvard economist Michael Porter’s research in the ’70s and ’80s shed doubts on the idea of synergy, and Jack Welch was celebrated for running General Electric more leanly in the ’80s and ’90s. Stock valuation became more detailed as well, focusing on measurable aspects of a company like free cash flow as opposed to accounting abstractions like profit and revenue.

That decade’s lessons of ravenous acquisition were learned perhaps most harshly by LTV and its investors, but their tale of unsustainable growth seems to be renewed with each bubble or boom. History doesn’t repeat itself, but injurious investment banking does.

Myriad opportunities for value and technological growth in the postwar years turned into decades of income stagnation and inequality, largely because of the high-stakes games played by conglomerates. “It’s easy to talk yourself into a deal that makes you and people you know lots of money, but actually harms the company,” Hyman says. In the case of James Ling, clever finances took precedence over production and innovation.

Contrary to the Post’s prediction fifty years ago, the entire United States did not become one vast conglomerate presided over by James Ling. Conversely, the Texan has been largely forgotten by anyone unfamiliar with the annals of American business. His philosophy of rushing for quick money over good economy, however, remains an enduring trope.

Become a Saturday Evening Post member and enjoy unlimited access. Subscribe now

Comments

This is one of the most simultaneously fascinating and frightening stories I’ve ever read, period. I appreciate the 1968 link, and the one on Louis Hyman’s new book. I’m ordering it soon. At least I’ll have a better understanding of the economically shark infested waters I’m swimming in, and can’t escape.

Meanwhile, these are TREMENDOUS amounts of money Ling had control over. You might as well swap out the word millions and replace it with billions in 2018 to grasp the magnitude of it now.

His crash and burn no doubt played a larger role in the ‘Sinking ’70s’ after the ‘Soaring ’60s’; the unsustainable highest high point of the 20th Century in nearly every way, economically for the masses. No doubt Ling benefited from the blood money the Vietnam War pumped into the economy during the LBJ years, combined with the lingering strength of the post World War II economy otherwise, of course.

Ling and the great economy for the masses were on their way out in 1970. Nixon’s final round of bombings in December 1972 ended Vietnam. In 1973, with the war over and the oil ‘crisis’ starting, the ’60s economy was replaced with terrible instability ever since, except for the wealthy. This was the beginning of the stagnant wages combined with inflation (stagflation) we have to this day, and will continue to.

All the extremism of what “rich” is, is sooo gluttonous now, even by Gilded Age standards of the late 1800’s and the rich of The Roaring ’20s. CEO pay that was then maybe 40 times higher than the average worker’s was in 1973, is what, 400,000 times higher now? I heard that recently.

College, of course, has been selling itself for decades as the ticket to the economic ‘promise land’. Hasn’t quite worked out that way, with a large percentage college grads (past and present) doing Uber, Lyft and more in this ‘Gig Economy’; sweatin’ it out with everyone else in the permanent peril of the American economic shark tank.